Think No Tax on Overtime? Not So Fast, Says the IRS

- Contact ILS

- Jan 22

- 4 min read

As the 2026 tax season approaches, discussions about the so-called “No Tax on Overtime” are shifting from theoretical to practical. In early November 2025, ILS released a detailed analysis of the One Big Beautiful Bill (OBBB), outlining how tip and overtime payments may qualify for federal tax deductions. This update focuses on clearing up common misconceptions about the overtime provision and helps employers understand how to prepare for both the current and future tax seasons.

If you or your company need support navigating overtime classification, W-2 reporting fields, or employee communications, please contact the ILS legal team at contact@consultils.com.

What It Really Means: A Federal Income Tax Deduction, Not “No Tax on Overtime”

The OBBB introduces a new federal income tax deduction mechanism tied to overtime pay—commonly misunderstood as “overtime tax exemption.” Here’s the actual structure:

Applicable Period: January 1, 2025 through December 31, 2028

Deduction Cap: Eligible individuals can deduct up to $12,500 in qualified overtime pay from their federal income taxes per year. Married couples filing jointly may deduct up to $25,000.

Income Phase-Out: For single filers, the deduction begins phasing out at a Modified Adjusted Gross Income (MAGI) of $150,000 and is eliminated at $275,000. For joint filers, the phase-out begins at $300,000 and ends at $550,000.

Filing Conditions: The deduction is available whether the taxpayer uses the standard or itemized deduction, as long as a valid SSN is listed on the return. Married individuals generally must file jointly to claim it.

The most important employer takeaway: This is a deduction applied by the employee on their tax return. It does not change the employer’s payroll tax responsibilities, withholding obligations, or reporting duties.

Three Common Misunderstandings About the “No tax on Overtime”

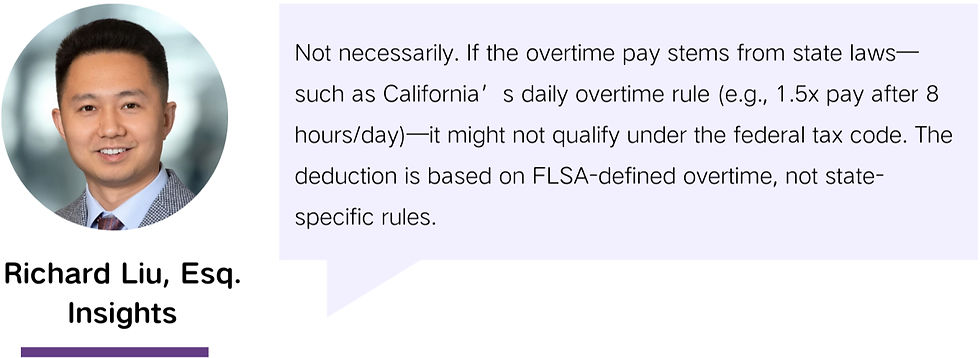

Myth 1: All overtime qualifies for tax deduction

Just because you paid overtime under state law doesn’t mean the IRS will count it for the deduction.

Myth 2: Employees can deduct the full amount of their overtime pay

Myth 3: Since it’s “tax-exempt,” employers can withhold less

Real-World Employer Challenge: The Hard Part Is Systems and Reporting

For employers, the biggest challenge under OBBB is data governance and information reporting—not interpreting the tax rule itself. You’ll need to:

Track and report qualified overtime pay accurately (potentially on W-2 forms),

Coordinate among Payroll, HR, and Finance on definition and classification,

Educate employees and avoid miscommunications like “overtime isn’t taxed.”

This breaks down into three operational hurdles:

Definitional Consistency: What counts as “qualified overtime pay” across different states and roles?

System Capability: Can your current payroll or HRIS system extract and tag this data for W-2 reporting?

Employee Messaging: How do you explain this to employees without causing confusion or misaligned expectations?

IRS Enforcement Signal: Expect Heavier Compliance in 2026 and Beyond

According to IRS Notice 2025-62, the IRS is offering a one-year grace period in 2025 for employers who are still updating systems. If employers haven’t yet created separate line items for “qualified overtime pay” and “qualified tips,” they may qualify for penalty relief as long as the overall reported figures are accurate and complete.

That doesn’t mean you can underreport. The total wages—including qualified overtime—must still be reported in full.

Also, W-2 and 1099 forms will not be updated for 2025 to accommodate the new deduction. Instead, the IRS encourages employers to deliver supporting information via:

W-2 Box 14 notations,

Employee portals,

Supplementary written statements.

These are recommendations, not mandatory, for penalty relief.

Action Plan for Employers & HR Teams

To reduce compliance risk and smooth communications during tax season, employers should consider these action steps:

Define “Qualified Overtime Pay” Internally: Use FLSA standards, with notes on how to handle state-specific rules.

System Review: Check if your payroll or HRIS can add and extract “qualified overtime” fields for W-2 use.

Document the Process: Build an audit trail for how data is collected, reviewed, and shared with employees.

Unify the Messaging: Train HR to describe this as a “potential income tax deduction”, not “tax-free overtime.”

Conduct Internal Training: Ensure HR, Payroll, Finance, and front-line managers understand recordkeeping, approval, and reporting processes.

To revisit ILS’s original OBBB policy analysis from November 2025, click here for

more detailed information. For help implementing these new requirements—whether you need support with overtime classification, W-2 reporting fields, or internal communication strategy—reach out to our legal team at contact@consultils.com. We’re here to help you stay compliant and avoid costly surprises.

Disclaimer: The materials provided on this website are for general informational purposes only and do not, and are not intended to, constitute legal advice. You should not act or refrain from acting based on any information provided here. Please consult with your own legal counsel regarding your specific situation and legal questions.

As Managing Partner at ILS, Richard Liu ranks among the leading U.S. attorneys in corporate, employment, and regulatory law. He is known for crafting legal strategies aligned with clients’ business objectives and advising Fortune 500 companies, startups, and executives on corporate transactions, financing, privacy, and employment matters across the technology, healthcare, and financial sectors.

Before founding ILS, Richard practiced at top defense firms, where he developed a reputation for anticipating risks and designing strategies that balance protection with growth. He has secured favorable outcomes in contract and intellectual property disputes, represented clients in state and federal courts, and is recognized for combining large-firm expertise with boutique-firm agility. Richard is also a frequent speaker at industry and legal conferences.

Email: contact@consultils.com | Phone: 626-344-8949-8949

Comments